We are in a state of expectation, with plenty of fundamental 'noise' to cause short-term volatility. Retail traders' appetites for sole technicals or the belief that every event risk has equal potential might lead to hazardous exposure. When it comes to the markets, however, there is a hierarchy of power, and the most significant event typically commands the largest potential for market movement. This is especially true in the run-up to its release since anticipation brings with it a plethora of possibilities and potential degrees of effect. We are completely focused on the importance of the FOMC rate decision on Wednesday, and the activity we have seen so far this week is most certainly a reflection of that perspective.

On a technical basis, the surge through the US indexes this week managed to achieve substantial headway. For the first time in 203 trading sessions, the Nasdaq 100 closed above its 200-day simple moving average (SMA), catching up to its bigger competitors. Monday, the index fell again below that ostensibly key threshold. The -1.3 percent drop in the S&P 500 was a significant reversal that returned the market to the top of the last resistance band, which was around 4,030-4,020. What stands out to me is that, despite January's bumpy (up to 6.7 percent) improvement, participation has all but stalled. Using e-mini S&P 500 futures and options open interest as a proxy for broad speculative activity, there has been no discernible rebound after the December FOMC decision.

S&P 500 E-mini Futures Chart with 200-Day Simple Moving Average, Volume, Open Interest, and 1-Day ROC (Daily)

The erratic market activity we are presently seeing is a result of expectation, and a quick peek at the economic calendar explains why. The FOMC rate decision, due at 19:00 GMT Wednesday, will speak to monetary policy's global outlook.

While the US central bank did not raise at the quickest rate among its peers, and may not go as far as some of its peers, it is a leader of the current tightening regime, as it was the unconventional stimulus of the previous period of monetary policy. If the central bank indicates that it will continue to tighten to its goal 'terminal rate' despite low inflation, the effect will be felt across the risk markets. If they announce an unexpected halt, the effect will be just as wide but considerably more severe ('risk on' in this scenario). As we near the end of January and await the Fed's decision, there is still a major event risk on the horizon.

Top Global Macroeconomic Event Risks for Next Week

This session's emphasis will be mostly on growth-oriented measures. The first item is a worldwide one in the IMF's World Economic Outlook update (WEO). In the last month, IMF Director Georgieva has indicated that the global economy's projection has improved, which seems to be in line with the market's recent discount. Should that excitement fail to materialize, it is likely to weigh on the market's mood – albeit this history is not one that can be depended on to cause significant volatility. Nonetheless, it influences the understanding of the following facts and occurrences on the same issue. China will provide the other Asia session growth report, with the NBS PMI and industrial earnings likely to be released. There will be a series of advanced 4Q GDP reports from important Eurozone economies in Europe, but the Eurozone gauge will carry the most weight. Mexico and Canada will release their own GDP figures during the North American session, but the Conference Board's consumer confidence survey from the US docket will feed into the composite of the US basic picture that we will create this week.

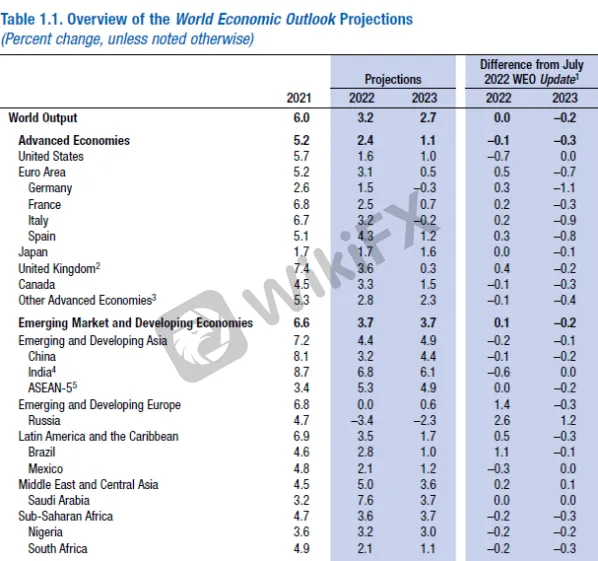

The IMF's Forecast for Global Growth

Given the greater market expectation this week as we exchange one event for another on consecutive days, it is crucial to note that the United States will confront a particularly overwhelming sequence of diversions this week. We have the ISM manufacturing survey and the previously stated consumer confidence data before the FOMC decision; following the announcement, we will go over FAANG profits, NFPs, and the ISM's service sector activity report. If you're looking for a severe break in the DXY Dollar Index, look for a technical break from the fairly tight trend channel the currency has carved over the last two weeks. Despite a modest advance upward this session, the increase will not even widen the exceedingly small 1.37 percent range over the previous 11 trading days. While this is focusing on the index, anticipate the same type of fight for the EURUSD, GBPUSD, and USDJPY lies. Furthermore, given the ECB and BOE rate decisions on Thursday, the complexities for EURUSD and GBPUSD are significantly larger.

DXY Dollar Index Chart with 200-Day SMA and 11-Day Historical Range (Daily)

Stay tuned for more Market news.

Install the WikiFX App on your smartphone to stay updated on the latest news.

Download link: https://www.wikifx.com/en/download.html

Leave a Reply