Sequel to missing their annual Santa Claus run in 2022 and starting the New Year in the red, US stocks registered significant gains this week to snap out of their 4-week bear run.

Forex

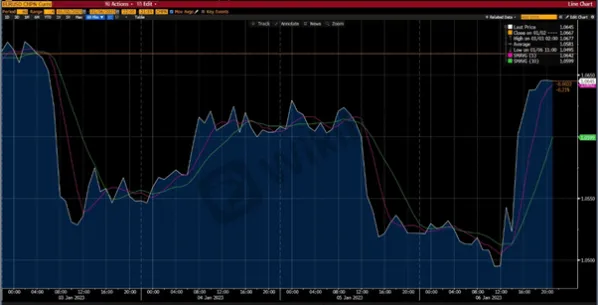

The EUR/USD closed the week on a strong footing as the US dollar couldnt capitalise on the encouraging non-farm payrolls (NFP) data released on Friday, 6 January. The report by the Bureau of Labour Statistics (BLS) revealed a rise in NFP by 223,000 and a 3.5% decline in unemployment rate in December. It also showed a decrease in annual wage inflation from 4.8% to 4.6%.

Moreover, the Institute for Supply Managements Services Purchasing Managers' Index (PMI) survey — released on Friday, 6 January — showed a contraction in the services sector during December. These releases contributed to the 10-year US Treasury bond yield losing more than 4% on the day, resulting in heavy selling pressure on the US dollar that capped its possible upward movement.

Meanwhile, the British pound sterling continued its strong run, which led to the GBP/USD pair posting its biggest daily jump for the week on Monday, 2 January, before ultimately closing at $1.21. A price cap on energy prices in the United Kingdom has contributed towards an ease in inflation, bolstering the pound.

This week will see the release of the Consumer Price Index (CPI) data in the United States on Thursday, 12 January. Meanwhile in the United Kingdom, the gross domestic product (GDP) and the manufacturing production data will be released on Friday, 13 January.

Level up your trading strategy with the latest market news and trade CFDs on your Deriv X account.

Commodities

Gold prices continued their bullish run to end last week at $1,866, flirting with their highest level in 7 months. The selling of the US dollar, despite encouraging jobs data, downbeat PMI numbers, and the fall in treasury bond yields all contributed to the rise in the price of the yellow metal.

Amid the surge in prices of the commodity, China reported an increase in its gold reserves for a second straight month, having raised its holding by 30 tonnes in December 2022 and by 32 tonnes in the month prior. The total gold reserves in China now stands at 2,010 tonnes.

Last week, both the major oil benchmarks — West Texas Instruments (WTI) and Brent — dropped over 8% to register their biggest declines at the start

of a year since 2016.

Oil prices were impacted by the fears of a rise in Covid infections in China as the country opened its borders for the first time in 3 years. The resulting increase in travellers could lead to an increase in Covid cases. If such a scenario were to materialise, it could potentially lead to a lack of demand for oil. Meanwhile, Saudi Arabia slashed the price of its oil sold to Asia and Europe in February 2023, signalling concerns of a slowdown in demand in the near-term.

Cryptocurrencies

Cryptocurrency price movement was slow at the start of the week due to the holiday season, but it picked up pace later in the week to finish strongly. The global cryptocurrency market capitalisation crossed the $850 billion mark on Sunday, 8 January.

The worlds largest cryptocurrency, Bitcoin, started trading above the $16,800 level on Wednesday, 4 January, as market volatility remained high. Bitcoin breached the $17,000 mark last week and was trading at $17,068 on Sunday, 8 January. Ethereum, the second-largest cryptocurrency in the world, was trading at $1,290 at the time of writing.

In an interesting turn of events, the United Kingdom has enforced a tax exemption for foreign investors buying cryptocurrencies through local investment managers or brokers. The tax break is a part of Prime Minister Rishi Sunak's plans to turn the United Kingdom into a cryptocurrency hub, and will lend credibility to the industry.

Meanwhile in the US, the bankruptcy team of Future's Exchange, commonly known as FTX, has agreed to coordinate with liquidators who are winding down the exchange's operations in the Bahamas, resolving a dispute that threatened the recovery of billions of dollars in lost funds.

Take advantage of market opportunities by sharpening your trading strategy and trading the financial markets with options and multipliers on DTrader.

US stock markets

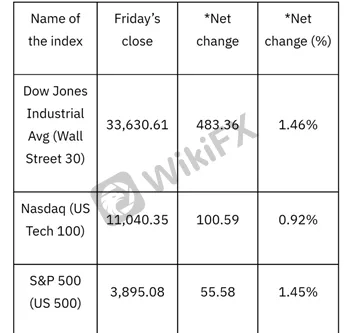

Net change and net change (%) are based on the weekly closing price change from Friday to Friday.

The encouraging jobs data in the United States lifted Wall Streets gloom as major stock indices finished the week with substantial gains, ending a month-long bearish run. The Dow Jones Industrial Average rose 1.46% to close at 33,630.61, the S&P 500 gained 1.45% to end at 3,895.08, and the Nasdaq Composite was up by 0.92% to finish the week at 11,040.35.

The upbeat NFP data fuelled belief among investors that inflation is decreasing and that the US Federal Reserve will tone down its aggressive stance on interest rates. Since the March 2022 quarter, the Fed has increased rates 4.50% cumulatively from 0.25%.

However, the likelihood of a Fed rate hike remains high as Atlanta Fed President Raphael Bostic said that he expects the rates to rise above 5% and to stay there until “well” into 2024.

The CPI data as well as Federal Reserve Chairman Jerome Powell‘s remarks scheduled for Tuesday, 10 January, will be closely watched and will determine the course of the stock market movements this week. Now that you’re up-to-date on how the financial markets performed last week.

Leave a Reply